Bright value is the “normal “ form of extraction in which the flow is from peripheral labor and capitalists to core capitalists. Bright value is based on normal bookkeeping in which all paid out costs are worked out and recorded. Should these costs be at world market values, the drain of value, through repatriation of profits, is similar to ordinary drains within the core. However, drains from periphery to core are more likely to be of long duration, thus leaving control of investment of the surplus in the hands of the recipient. More interesting are the cases of “super-exploitation” in which the recorded costs are below world market values, causing the difference between these costs and competitors’ costs is the source of monopoly profit that is transferred to the core. It is important to note that such drains occur between internal peripheries and their cores. I designate this form of value as “bright” because (a) the costs are openly accounted, and (b) the surplus is collected by core capitalists.

Since bright value extraction drives the world-system, one might expect that massive research effort would have been applied to the analysis of the forms and extent of such transfers. Such is hardly the case. First, there are huge methodological difficulties. Second, to many, the demonstration of the existence of continuing polarization negates the importance of specifying the precise mechanisms of inequality. Third, for many, the world-economy is mostly an intra-core phenomenon since 80 percent of economic transactions are within the core. Fourth, there are numerous stories of peripheral survival and resistance.

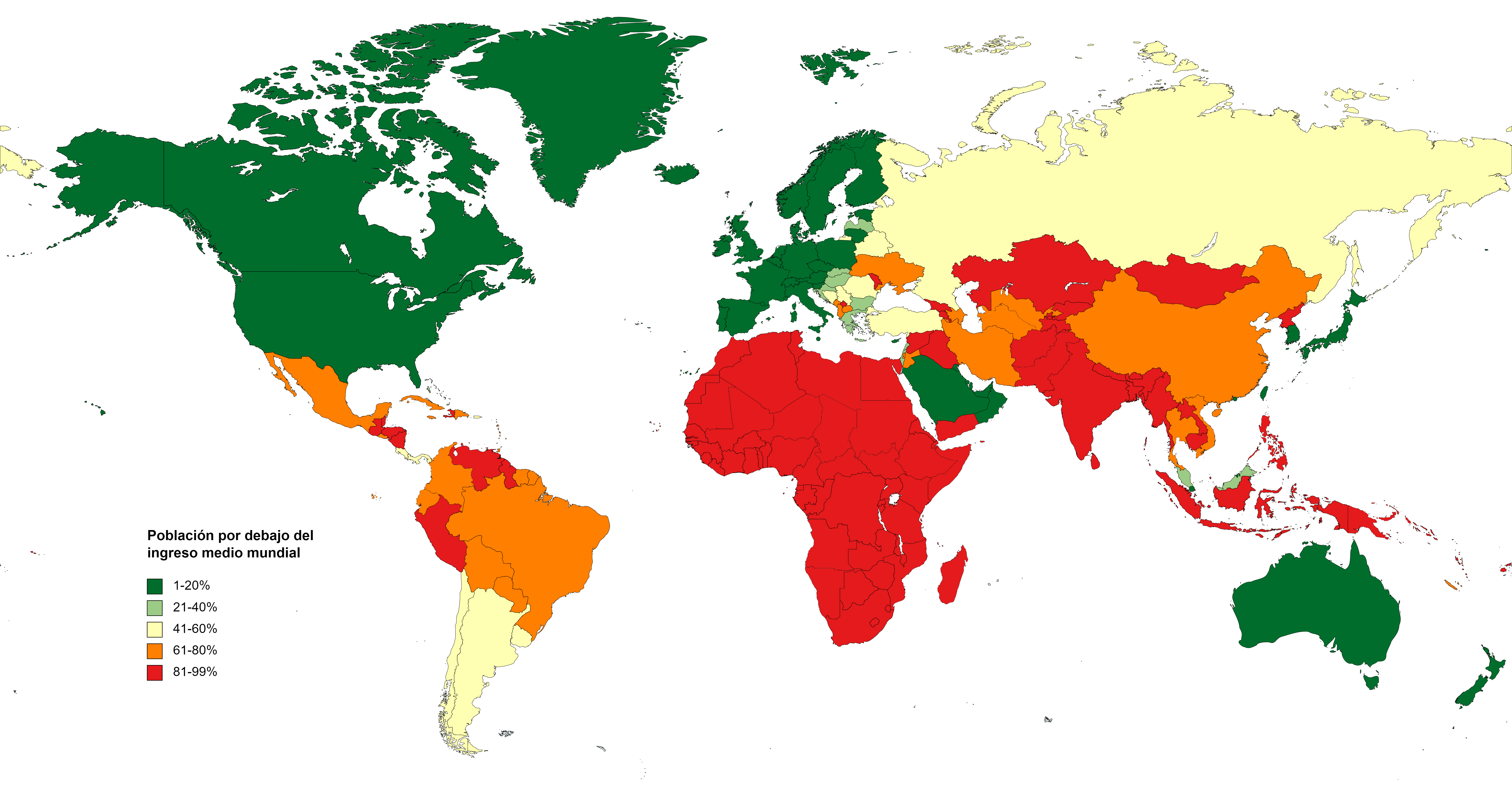

World-systems scholars only rarely attempt to devise estimates of the amount of drains from place to place in a given time period. Perhaps, it is sufficient to show that capitalists consistently have stimulated waves of capital, commodity, resource, and labor flows, always with the intent of returning surplus to the core, usually with the intent of obtaining super-profits. The increasing income gap between core and periphery (OPEC countries and newly industrialized countries excluded) may be explained as a result of surplus drain or as a result of variety of forms of developmental blockage, independent of any such drain. The latter are generally path-dependency arguments, more pessimistic versions of modernization theory. The more optimistic works, based on developmentalist theories, see growth occurring, inequalities being reduced and blockage being overcome by processes of convergence. It should be noted that the basic logic of surplus transfer theory does not imply the complete absence of development in all peripheries at all times. Part of the surplus available for expanded investment is always controlled by actors in the periphery so that there are large-scale accumulations in parts of the periphery, e.g., China today. The basic big picture quantitative work on surplus transfer shows that drains from the periphery are not large enough to explain major changes in the core. But these studies do not deny the cumulative advantage of drain to the core. Moreover they ignore transfers to internal core regions from internal peripheries and the peripheries of other core states. In addition, drains from peripheral zones to semi-peripheral zones is not addressed. The more basic question about surplus drain is its impact on the source. Looking up from below, it appears that most surplus is lost forever. Even though enough surplus should be retained to stimulate growth, what has been lost remains a lost opportunity cost. Potential advantages of economic multipliers and innovative investment have been exported along with the surplus.

Mechanisms of Bright Value Drains from the Production Process

Foreign Direct Investment always has been a major source of surplus drain. This occurs through the immediate repatriation of profits or longer term repatriation after years of expanded reinvestment. Investment in the periphery is at higher risk than in the core. It is even more a search for a degree of monopoly. The vast majority of FDI has been core on core; it is rarely noted that most of this investment is centered within internal peripheries. Most peripheral FDI occurs in order to establish control of resources or to cut production costs for exports. Before the last half-century, FDI was basically oriented toward insuring the availability of resources and energy needed for production at home and for exports to core markets and toward the production of agricultural exports. Recently, there has been a turn toward manufacturing FDI largely for export. There has been a huge expansion in peripheral investment, particularly in China. Given China’s unique historical position as the only semi-peripheral workshop of the world, it is likely that this bright value drain from the core will continue. If so, the basic structure of the world-system will be significantly different from all previous arrangements.

Other forms bright value drain related to production include the payment of fees for intellectual property rights and fees for services. A minor form of drain that has long irritated locals is the repatriation of salary-based savings of foreign personnel and their tendency to spend their salaries on imports from their home countries.

Mechanisms of Bright Value Drains from Commerce

It is generally thought that the long history of trade in luxury goods did not entail much surplus drain. The profits were reaped from the monopoly of transportation routes and a sales monopoly in the home market. Such quasi-monopolies are common today in luxury goods, but are doubly enhanced because of the lower costs of peripheral production. Multinational corporations also put great effort into promoting brand-name monopoly, thus higher prices, in the periphery, the same practice as indulged in the core, but resulting in bright value drain. WalMart and others have improved on this practice by establishing monopsony control of sellers at the producers end of the commodity chain while maintaining a high degree of monopoly at the retail end.

What were once called commodity chains, a central world-systems concept (Wallerstein, 1983), now are commonly designated as “global value chains” which are not conceptualized as draining surpluses from exploited countries to richer core and semiperipheral zones. Omitting all of Wallerstein’s (1983) of exploitation, this mainstream approach focuses attention on value added at each step in the chain and contends that countries can develop strategies to collect more profits from the chain. In my view, however, surplus drain and exploitation should be kept at the conceptual heart. such chains between independent buyers and sellers exist as an alternative to internalized production chains within multinational corporations. The multinational corporation has increased its outsourced transaction “costs” by externalizing its production chain as a trade chain. It does so in order to reduce costs, thus obtain “transaction benefits”. Much of the value added at various steps in the chain is added to the surpluses collected toward the end of the chain. In other words, commodity chains are “degree of monopoly chains”, designed to transfer surplus from competitive capitalists to quasi-monopolist capitalists, generally higher up the chain and in the core.

Mechanisms of Bright Value Drains from Finance

Important bright value transfer mechanism are the loans provided to the periphery by core institutions, including direct loans and bonds floated by peripheral states. Since leveraged productive investment lies at the heart of core capitalism, it seems reasonable that the periphery should be allowed a piece of this action. But being of a higher risk, the periphery is faced with a 2 percent minimum surcharge. Borrowing at the standard world rate,. over the long haul, should work out to the advantage of the borrower. Otherwise, such a system would have long since faded. There are numerous cases in which loans worked out as expected, but what comes to mind are the many cases of debt crisis. In recent years, the IMF, the core-controlled lender of last resort, has bailed out the core lenders in the name of providing relief to the peripheral borrowers. One of the few beneficial results of IMF conditionality policies is that most peripheral countries (the European semi-periphery excluded) have turned from core loans to the building of dollar reserves. Thus, the IMF has injured one of the geese that lays the golden eggs. In a massive historical reversal, China now lends money to the U.S., largely by buying treasury bonds, thereby keeping the over-leveraged U.S. economy afloat. In this case it may be argued still that the surplus flow is to the core, as the Chinese “investment” will eventually be paid off in vastly cheapened dollars.

Other forms of financial bright value surplus drain include portfolio investment, capital flight, and exchange rate manipulation and speculation. Portfolio investment in peripheral enterprises involves the shift of dividends and realized capital gains to the core. Such transfers have only rarely been an important component of surplus drain. Capital flight is the transfer to the core of peripheral surplus by peripheral capitalists. The damage of such drains to the periphery vastly exceeds any advantages to the core. Exchange rate speculation can very rapidly devalue the paper wealth of a nation and exchange value of its exports, causing a massive surplus drain through currency flight and loss of export revenues.

References Cited

- Wallerstein, Immanuel. 1983. Historical Capitalism. London: Verso.